One of the most underused features of the VA home loan program is the ability to purchase multi-unit properties as long as one of them is your primary residence. Veterans can buy a duplex, triplex, or fourplex with a VA-backed purchase loan and zero down payment, then rent the units you’re not living in to offset or even fully cover their monthly mortgage.

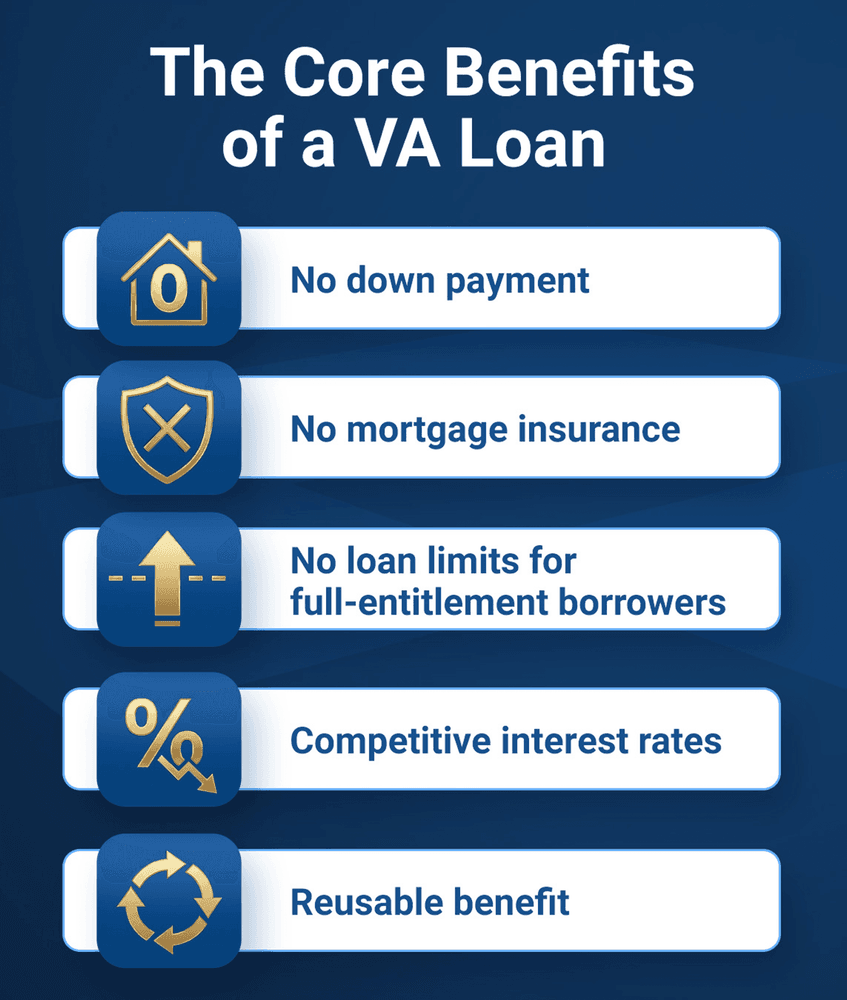

The same core VA benefits apply: no private mortgage insurance, competitive interest rates, and flexible underwriting standards.

However, multi-unit purchases come with additional requirements that single-family transactions do not.

- The Veteran must occupy one unit as a primary residence.

- Rental income is counted toward qualification, but only at a discounted rate.

- For three- and four-unit properties, many lenders apply a self-sufficiency test that the property must pass before the loan can be approved.

The Occupancy Requirement

The VA loan program is built around owner occupancy. To use a VA loan for a multi-unit property, the Veteran must intend to live in one of the units as their primary residence. This is not optional and it is not a technicality. Misrepresenting occupancy intent is considered fraud and can result in loss of VA loan benefits.

Veterans are generally expected to move into their unit within 60 days of closing. Active-duty service members with deployment or PCS timing issues may receive some flexibility, but the intent to occupy must be documented at the time of application. After satisfying the occupancy requirement (typically 12 months of living in the property), the Veteran may later convert the home to a full rental and potentially use remaining entitlement to purchase a new primary residence.

How Rental Income Is Counted

Rental income from the non-owner-occupied units can be used to help the Veteran qualify for the loan. This is a significant advantage because the added income can substantially increase borrowing power and lower the effective debt-to-income ratio.

However, lenders don't count 100% of the expected rent. The standard practice is to use 75% of the projected or actual rental income from the other units. The 25% discount accounts for vacancy, maintenance, and collection risk. If a second unit in a duplex rents for $2,000 per month, the lender would count $1,500 toward the Veteran's qualifying income.

For existing properties with tenants already in place, the lender uses the current lease agreements. For vacant units or new purchases without established leases, the VA appraiser provides a fair market rent estimate as part of the appraisal report. The lender then applies the 75% factor to that figure.

Some lenders add their own overlays on top of this. A few require the borrower to have prior landlord experience before counting rental income, and others may use a lower percentage than 75%. Working with a lender experienced in VA multi-unit transactions matters here because policies vary.

The Self-Sufficiency Test for Three- and Four-Unit Properties

For triplexes and fourplexes, many lenders apply a self-sufficiency test. This test requires the total rental income from all units, including fair market rent on the unit the Veteran will occupy, to cover the full monthly mortgage payment (principal, interest, taxes, and insurance). If the property doesn't pass, the lender may decline the loan regardless of the Veteran's personal income.

This is a lender overlay, not a VA requirement, but it appears frequently enough that Veterans shopping for three- and four-unit properties should treat it as a practical hurdle. Duplexes are generally exempt from this test, which is one reason they are the most common multi-unit VA purchase.

Running the self-sufficiency numbers before making an offer is the simplest way to avoid wasting time on a property that won't qualify. Your lender or real estate agent can help estimate the calculation using the appraiser's rent schedule and the projected PITI.

Entitlement and Loan Limits

For Veterans with full entitlement, meaning they have never used their VA loan benefit or have fully restored it, there is no VA-imposed loan limit. The maximum loan amount is whatever the lender approves based on the Veteran's income, credit, and the property's appraised value.

For Veterans with partial entitlement, meaning they already have an outstanding VA loan, county loan limits come into play. These limits determine how much the VA will guarantee for a zero-down purchase. The VA instructs lenders to use the one-unit conforming loan limit for entitlement calculations, even on multi-unit properties. In most counties for 2026, the baseline one-unit limit is $832,750, though high-cost areas have higher ceilings.

If the loan amount exceeds what the remaining entitlement can support, the Veteran may need to make a down payment to cover the guaranty gap. Confirming entitlement status early with a Certificate of Eligibility is important for multi-unit buyers because property prices for duplexes, triplexes, and fourplexes are typically higher than single-family homes.

The VA Funding Fee on Multi-Unit Purchases

The VA funding fee applies to multi-unit purchases at the same rates as single-family homes. For a first-time user making no down payment, the fee is 2.15% of the loan amount. For subsequent use with no down payment, it rises to 3.30%. The fee can be reduced with a down payment of 5% or more, and it can be rolled into the loan balance.

Veterans receiving VA disability compensation, certain Purple Heart recipients on active duty, and qualifying surviving spouses are exempt from the funding fee entirely. Given the higher loan amounts typical of multi-unit purchases, confirming exemption status before closing can represent significant savings.

What the Appraisal Covers

The VA appraisal on a multi-unit property is more involved than a standard single-family appraisal. The appraiser evaluates the property using an income approach in addition to the standard comparable sales approach. This means the appraiser considers the rental income the property generates (or could generate) alongside what similar properties have sold for in the area.

The appraiser also provides a fair market rent estimate for each unit, which feeds directly into the lender's rental income calculation and the self-sufficiency test. Each unit must meet the VA's Minimum Property Requirements for safety, structural soundness, and habitability. If any unit has health or safety issues, repairs may need to be completed before closing.

The VA home loan eligibility page outlines the broad framework for VA loan qualification, including the property standards that apply to all VA-financed homes.

Practical Considerations Before Buying

Multi-unit properties offer real financial advantages, but they come with responsibilities and costs that single-family homes do not.

Property management is part of the deal. Even if you live next door to your tenants, you are a landlord. That means handling maintenance requests, collecting rent, managing vacancies, and complying with local landlord-tenant laws.

Insurance and taxes are higher. Multi-unit properties carry higher property tax assessments and require landlord insurance policies that cost more than standard homeowner's coverage. These costs are included in your PITI and affect your qualifying ratios.

Reserves may be required. Some lenders require cash reserves, typically three to six months of mortgage payments, for multi-unit VA purchases. The VA itself does not mandate reserves for owner-occupied multi-unit properties, but lender overlays are common.

Not every market has inventory. Multi-unit properties are less common than single-family homes in many areas. In competitive markets, they sell quickly and often attract cash investors. Working with a real estate agent familiar with multi-family inventory gives you a meaningful advantage.

The CFPB's guide to debt-to-income ratio is a useful reference for understanding how HOA fees, insurance, taxes, and rental income interact with your qualifying ratios.

Thinking about buying a multi-unit property? Learn more about VA loan options and qualification.

FAQs

Can I buy a fourplex with zero down using a VA loan?

Yes. Veterans with full entitlement can purchase a property with up to four units with no down payment, as long as they occupy one unit as their primary residence and the loan meets lender qualification requirements.

How is rental income counted for VA loan qualification?

Lenders typically use 75% of the projected or actual rental income from the non-owner-occupied units. The 25% discount accounts for vacancy and maintenance. Some lenders apply additional overlays, such as requiring prior landlord experience.

What is the self-sufficiency test?

Many lenders require that the total rental income from all units, including fair market rent on the owner's unit, cover the full PITI payment. This test is most commonly applied to triplexes and fourplexes. Duplexes are generally exempt.

Do I have to live in the property?

Yes. The VA requires that you occupy one unit as your primary residence, typically within 60 days of closing. After meeting the occupancy requirement, you may later convert the property to a rental and use remaining entitlement for a new purchase.

Are VA loan limits different for multi-unit properties?

The VA uses the one-unit conforming loan limit for entitlement calculations, even on multi-unit properties. Veterans with full entitlement have no VA-imposed cap. Veterans with partial entitlement should check county loan limits to determine their zero-down buying power.