If you have a service-connected disability rating, you may not owe the VA funding fee at all. That single fact can save you thousands of dollars at closing, yet many Veterans go through the entire homebuying process without ever knowing they qualified for an exemption. Here's a straightforward breakdown of who qualifies, how to confirm your status, and what to do if you missed the exemption.

What Is the VA Funding Fee?

The VA funding fee is a one-time charge paid at closing on most VA-backed home loans. It exists to keep the VA home loan program self-sustaining, covering loan losses so the program can continue offering $0-down financing and no private mortgage insurance (PMI) to future generations of Veterans.

According to the U.S. Department of Veterans Affairs, the fee ranges from 0.5% to 3.3% of the total loan amount, depending on:

- Whether it's your first or subsequent use of the VA loan benefit

- Your loan type (purchase, cash-out refinance, or IRRRL/streamline refinance)

- How much, if any, down payment you make

For a first-time purchase with no down payment, the fee is currently 2.15%. On a $350,000 loan, that amounts to $7,525 due at closing, or rolled into the loan balance. Subsequent-use borrowers with no down payment pay 3.3%, or $11,550 on that same loan amount.

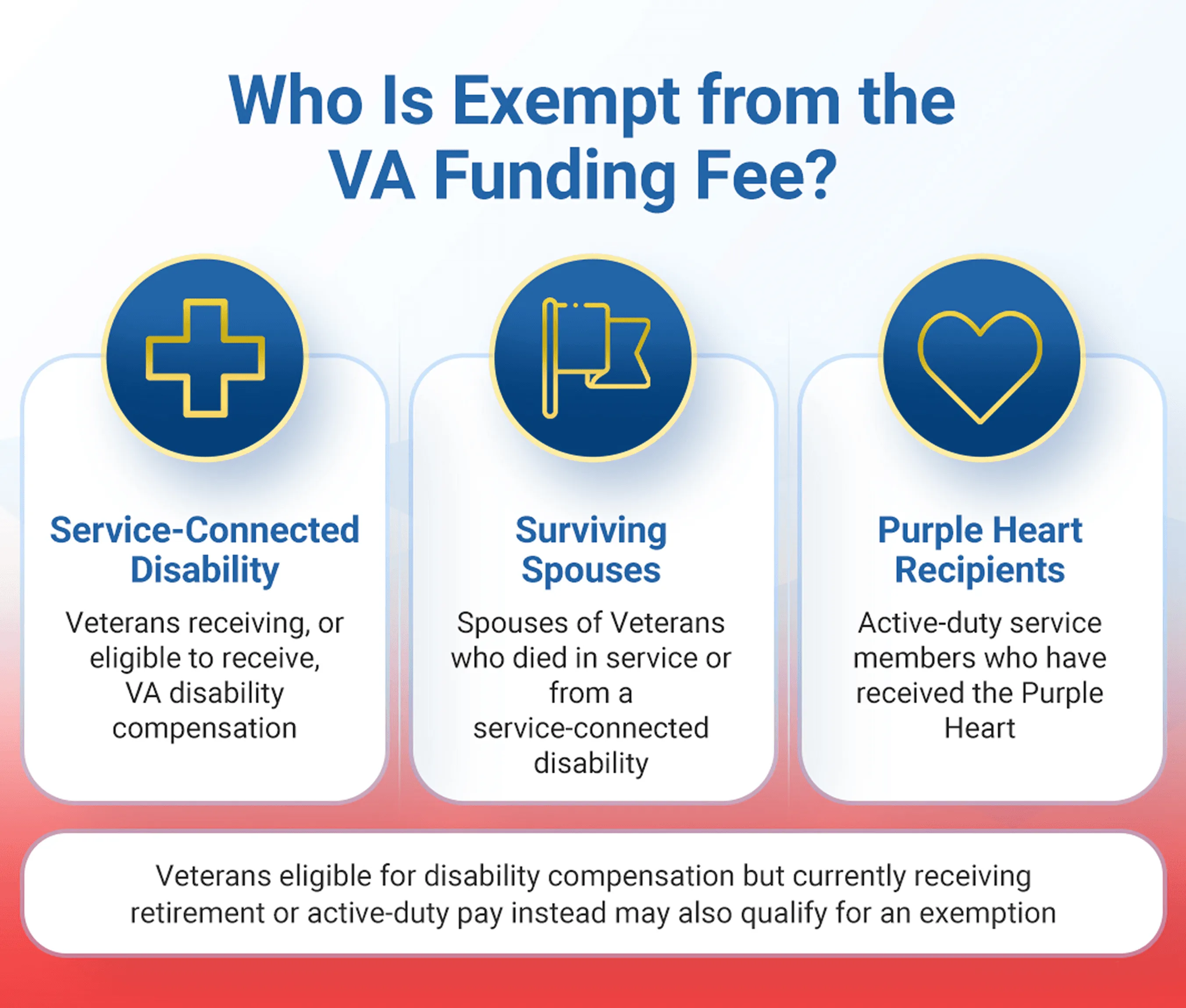

Who Is Exempt from the VA Funding Fee?

The VA funding fee exemption is granted by federal statute, not lender discretion. VA.gov outlines the following categories of borrowers who are not required to pay the funding fee:

- Veterans receiving VA compensation for a service-connected disability. There is no minimum rating threshold. Any confirmed, rated service-connected disability that results in VA compensation qualifies.

- Veterans entitled to disability compensation but receiving retirement or active-duty pay instead. If you chose military retirement pay over VA compensation, you may still qualify.

- Active-duty service members who received a Purple Heart on or before the loan closing date.

- Surviving spouses receiving Dependency and Indemnity Compensation (DIC) as a result of a Veteran's death in service or from a service-connected disability.

- Service members with a proposed or memorandum rating issued before closing, based on a pre-discharge disability exam.

The key phrase throughout is "on or before the closing date." Your disability status must be officially established in VA records by the time the loan closes.

How the Exemption Shows Up on Your Loan

When a lender pulls your Certificate of Eligibility (COE), the document will indicate one of three funding fee statuses: EXEMPT, NON-EXEMPT, or CONTACT RLC (Regional Loan Center). Lenders are required to check this status and must not charge the fee to borrowers marked exempt.

According to the VA Lender's Handbook, Chapter 8, lenders must also submit documentation of exempt status with the closing package. If there's any discrepancy between your COE and your actual disability status, VA Form 26-8937 (Verification of VA Benefits) can be submitted to the VA for clarification before closing.

Don't assume the lender caught it. Before you sign your Closing Disclosure, confirm the funding fee line item reflects your exempt status. If your exemption is not showing on the COE but you receive VA disability compensation, bring your VA award letter to your lender immediately and ask them to resolve the discrepancy before closing day.

What Happens If Your Claim Is Still Pending at Closing?

This is one of the most misunderstood parts of the exemption process. If you have a pending disability claim at the time your loan closes, you are not yet exempt. The VA requires an official rating on record, not an anticipated one. Your lender must collect the funding fee as if you were non-exempt.

However, if your disability claim is later approved with an effective date that falls on or before your closing date, you may be entitled to a full refund of the funding fee you paid.

That refund does not happen automatically. You have to initiate it. VA.gov notes that you should call your VA Regional Loan Center at 1-877-827-3702 to request the refund. As of July 1, 2019, any funding fee refund is paid directly to the Veteran, regardless of whether the fee was originally financed into the loan.

To process the refund, you will need:

- Your VA disability award letter showing the effective date

- Your Closing Disclosure showing the funding fee amount charged

Veterans with retroactive disability ratings who paid a funding fee at closing should follow up directly with the VA. Many are entitled to refunds and never receive them simply because they were unaware the option existed.

Special Cases Worth Knowing

Pre-Discharge Ratings

Active-duty service members approaching separation who have filed a pre-discharge disability claim can potentially qualify for the exemption if a proposed or memorandum rating is issued before the loan closes. If no rating has been issued by closing, the fee must be paid. Service members in this situation should contact the VA Regional Loan Center for guidance before closing, since the documentation path requires coordination between the VA and the lender.

Retirement Pay vs. Disability Compensation

Some Veterans choose military retirement pay rather than VA disability compensation because of the way the two interact under concurrent receipt rules. Per VA guidelines, if you would be entitled to receive disability compensation but are receiving retirement pay instead, you still qualify for the exemption. Your lender's file must reflect this status, so providing the relevant documentation upfront prevents delays.

Surviving Spouses

An eligible surviving spouse receiving DIC is also exempt from the funding fee. However, surviving spouse eligibility must be established in the loan file before closing. The VA Lender's Handbook notes that lenders are not required to resubmit documentation when the surviving spouse's status is already on file from the loan application.

The Financial Impact of the Exemption

To put the stakes in plain terms: on a $400,000 first-time purchase with no down payment, the standard funding fee of 2.15% equals $8,600. A subsequent-use borrower in the same scenario would owe $13,200 at the 3.3% rate. For an exempt Veteran, those amounts are $0.

When a funding fee is financed into a 30-year loan, that upfront cost also accrues interest over the life of the loan. The exemption eliminates both the upfront cost and the long-term interest on it.

VA Funding Fee Deductibility in 2026

One recent development worth noting: VA News announced in early 2026 that eligible borrowers can now deduct the VA funding fee on their federal taxes starting with tax year 2026, as part of a restored mortgage insurance deduction. For Veterans who paid the fee, this may reduce the net cost at tax time.

The deduction generally requires itemizing on Schedule A, so its value depends on your specific tax situation. Borrowers who qualify for the disability exemption and pay no funding fee have nothing to deduct, which is still the more advantageous position. For those who did pay, consulting a tax professional about how to document the deduction using your Closing Disclosure is advisable.

Ready to take the next step toward homeownership? Learn more about the VA loan process and benefits.

FAQs

Do I need a specific disability rating percentage to qualify for the funding fee exemption?

No. There is no minimum rating threshold in the VA's exemption rules. Any service-connected disability for which you are actively receiving VA compensation qualifies you for the exemption, whether your rating is 10% or 100%.

How do I confirm my funding fee exemption status before closing?

Your Certificate of Eligibility (COE) is the primary document lenders use. It will show your funding fee status as EXEMPT, NON-EXEMPT, or CONTACT RLC. You can apply for or view your COE through VA.gov. If your COE doesn't reflect your disability compensation status, provide your VA award letter to your lender and ask them to submit VA Form 26-8937.

Can I get a refund if I paid the funding fee and later received a disability rating?

Yes, if the effective date of your VA disability rating is retroactive to a date before your loan closing date. You must contact your VA Regional Loan Center at 1-877-827-3702 to request the refund. It will not be issued automatically.

Does the exemption apply to refinances as well as purchases?

Yes. The exemption applies to all VA loan types, including purchase loans, cash-out refinances, and Interest Rate Reduction Refinance Loans (IRRRLs). Your exempt status should be verified each time you use your VA loan benefit.

What if my lender charged me the funding fee even though I was exempt?

Contact your lender immediately with documentation of your exempt status, including your VA award letter. If the issue is not resolved, you can contact your VA Regional Loan Center or file a complaint through the Consumer Financial Protection Bureau.