A survey conducted on behalf of NewDay USA in early 2026 tells a story that should concern anyone in the Veteran homeownership space: most Veterans know the VA home loan benefit exists, but far fewer understand what it does. The gap between awareness and knowledge is keeping thousands of eligible Veterans out of homes they could already afford.

The good news is that the gap is closeable. And the data points exactly to where it needs to close.

What Most Veterans Know About How the Benefit Works

Image created for NewDay USA

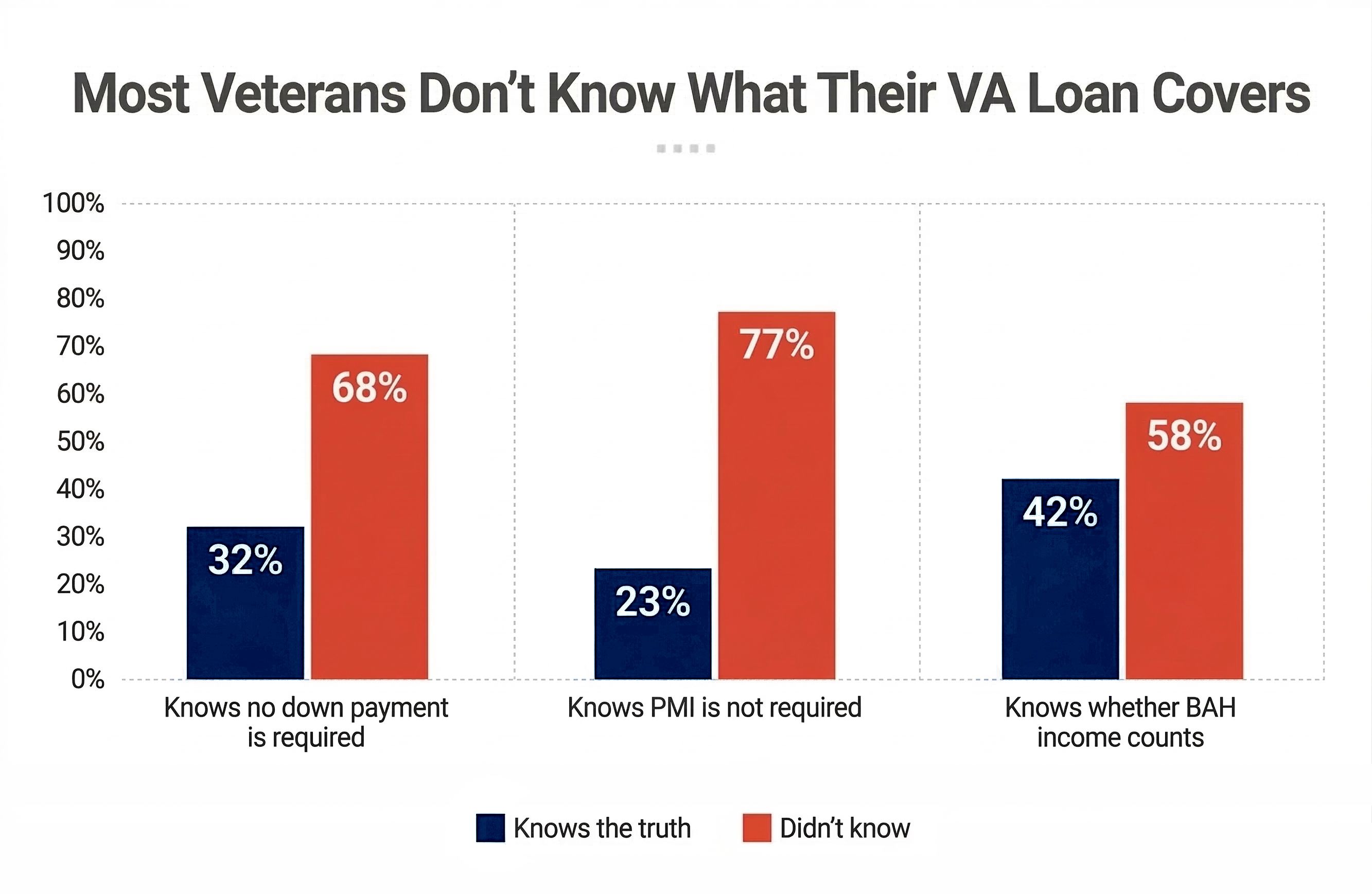

Sixty-three percent of Veterans surveyed said they are aware of the VA home loan benefit. That number sounds strong until you look deeper. Almost one in three (32%) said they were hardly educated or not educated at all about their VA home loan benefits during or after their military service. And 30% are unsure whether they qualify for the benefit at all.

- Only 32% knew that a VA loan requires no down payment

- 30% incorrectly believed a down payment is required

- 38% said they were simply unsure

There was even more confusion when it came to private mortgage insurance (PMI):

- Just 23% understood that VA loans do not require PMI regardless of down payment

- 30% believed PMI is required

- 47% said they had no idea either way

For Veterans who bypassed the VA loan because they assumed PMI was unavoidable and took out a conventional loan instead, that misconception can cost between $100 and $300 per month for as long as it takes to reach 20% equity.

The knowledge gaps extend further. Forty-two percent of respondents correctly knew that Basic Allowance for Housing (BAH) can count toward income qualification for a VA loan. But 39% were unsure, and 19% incorrectly believed it cannot be counted at all. For active-duty service members or recently separated Veterans, BAH can be a significant portion of total income. Not knowing it qualifies could lead someone to believe they earn less than they actually do for loan purposes.

The Four Myths That Keep Eligible Veterans From Homeownership

Myth 1: You Need a Down Payment to Use a VA Loan

This is the most consequential misconception in the data. The VA home loan guaranty allows eligible Veterans to purchase a home with no down payment, although individual lenders may have their own overlays.

When survey respondents were asked how much cash they thought they would need to buy a house using a VA loan:

- 19% said they were unsure

- 17% estimated $10,000 to $19,900

- 9% correctly answered none

These numbers explain a lot about why 49% of Veterans in the same survey reported feeling that homeownership is currently out of reach.

Myth 2: VA Loans Require Private Mortgage Insurance

Conventional loans require PMI when a borrower puts less than 20% down. VA loans do not require PMI at any down payment level. The VA's guaranty to the lender serves as a substitute for the insurance that PMI would otherwise provide. This benefit alone makes the VA a cost-efficient mortgage option for eligible borrowers.

Myth 3: VA Loans Are Slow to Close

29% of Veterans in the NewDay USA survey believed VA loans take longer to process than other mortgage types. This perception is outdated. Most VA loans close within a timeline comparable to conventional financing.

Myth 4: BAH Cannot Be Used to Qualify

- 42% knew BAH can count toward income qualification

- 39% were unsure

- 19% incorrectly believed BAH cannot be used to qualify

BAH is tax-free income, and lenders who understand VA guidelines will often gross it up when calculating qualifying income, effectively increasing its value in the underwriting process. Veterans and service members who are unsure how their income will be evaluated should ask their lender directly how BAH, disability compensation, and other military-specific income sources are treated.

VA Loan Costs

The VA home loan program does not require a down payment, up-front mortgage insurance, or monthly mortgage insurance, but there are some costs you should be aware of.

The highest cost is the VA funding fee, a one-time payment that helps sustain the program for future borrowers. For a first-time purchase with no down payment, the fee is 2.15% of the loan amount. For subsequent use, it rises to 3.3%. Veterans who put down at least 5% pay a reduced rate of 1.5%. The funding fee can be rolled into the loan balance rather than paid at closing, which preserves the no-out-of-pocket advantage. Veterans who receive VA disability compensation are exempt from the funding fee entirely, as are surviving spouses of Veterans who died in service or from a service-connected disability.

Beyond the funding fee, VA loan borrowers should expect standard closing costs, which can include

- The VA appraisal

- Credit report

- State and local taxes

- Title fees

- Real estate agent commission

- Recording fees

Lenders are also permitted to charge an origination fee capped at 1% of the loan amount. The VA prohibits lenders from charging borrowers a range of additional fees.

Even accounting for these costs, the VA home loan program remains a cost-efficient mortgage option for those who are eligible.

What Is Keeping Veterans From Buying

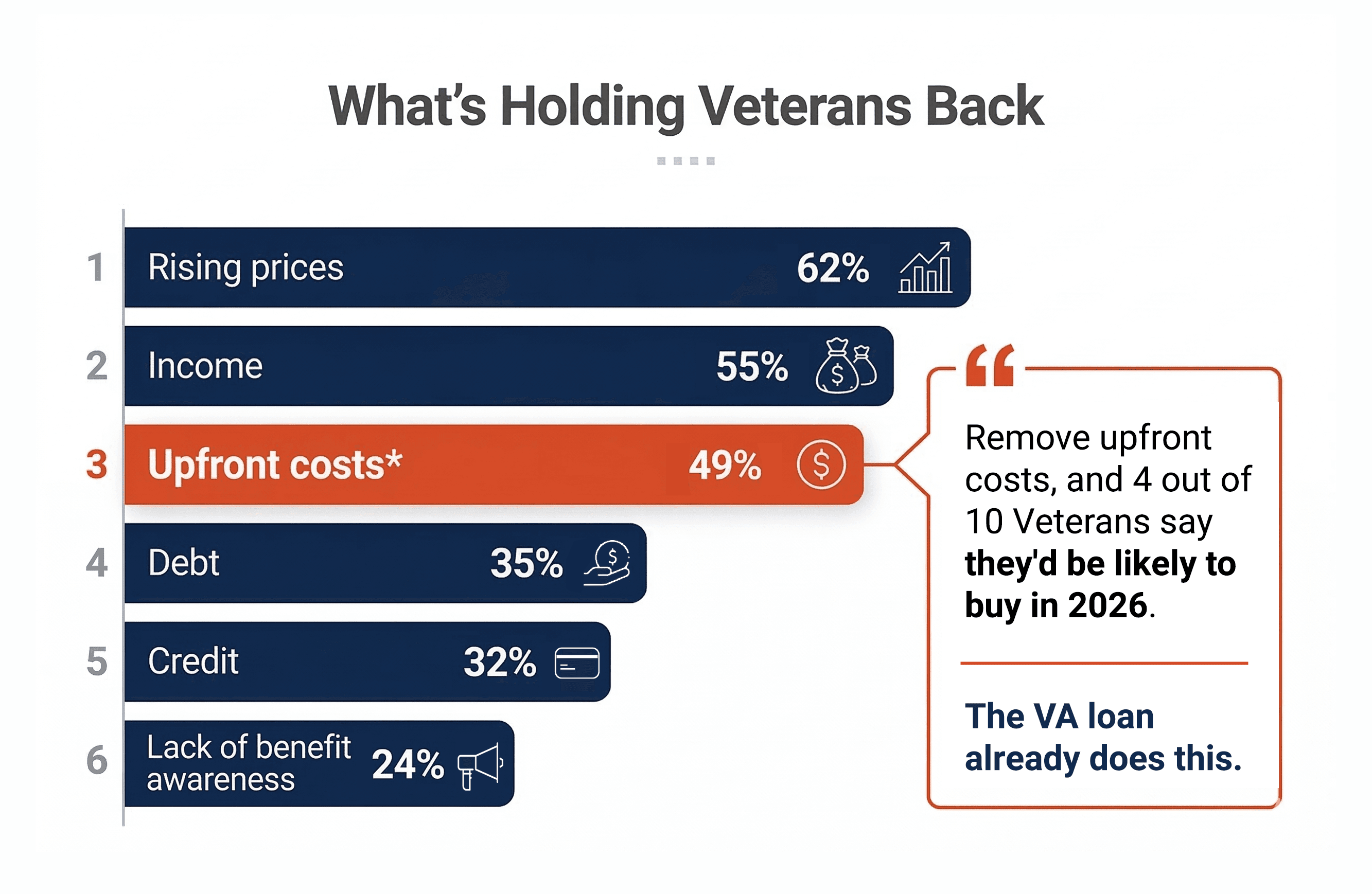

Rising home prices topped the list of perceived barriers survey respondents cited at 62%, followed by income concerns at 55% and saving for upfront costs at 49%. Debt obligations were cited by 35%, credit score concerns by 32%, and a lack of awareness about available benefits by 24%.

That last figure deserves a closer look. Nearly one in four Veterans identified a lack of awareness about benefits as a barrier to buying. This is an information problem, and one that the VA loan benefit is specifically designed to solve.

Only 21% of non-homeowners say they are completely or very likely to buy a home in 2026 when factoring in down payments and closing costs. Remove those costs entirely, and 40% of Veteran non-homeowners say they would buy a home. The VA loan already removes the biggest upfront cost: the down payment. Many people simply do not know that.

- 45% of respondents said they do not have enough savings to cover closing costs

- 35% have less than $5,000 saved toward those costs

- 18% have nothing saved at all

Image created for NewDay USA

What Homeownership Means to Veterans

The survey asked Veterans to describe what owning a home means to them.

- 64% said stability for their family

- 60% said personal freedom and independence

- 55% described it as a major life milestone

- 45% connected it directly to building wealth and investment

When asked how important owning a home is to increasing their net worth, 37% said it was extremely important, while 33% said it was very important. It’s clear that Veterans see a strong connection between financial security and homeownership, and the VA loan benefit is the most direct path to it for those who have served.

Understanding that a VA cash-out refinance can be used to pay down high-interest debt is another knowledge gap the survey surfaced.

- 28% of respondents reported carrying under $5,000 in high-interest debt

- 13% carried between $10,000 and $19,900

Only 36% of respondents knew that refinancing a home to take cash out was a debt payoff option at all.

Image created for NewDay USA

How Veterans Who Had Used a VA Loan Felt

Of Veterans who have previously purchased a home, 54% used a VA loan. Their experiences tell us a lot.

- 80% reported being highly satisfied with the process

- 47% said they would not have been able to buy their home without the VA loan

- 49% worked with only one lender to get approved

The most common challenges were:

- Delays in approval or processing (26%)

- Confusion about eligibility (25%)

- Difficulty understanding documentation requirements (24%)

The role of the real estate agent also showed up. 41% of respondents said their agent recommended a lender, making agent referrals one of the most common paths to choosing a VA lender.

What Veterans Can Do

Many Veterans also enter civilian life without a strong financial foundation to build from. 46% had less than $10,000 saved by the time they finished their military service, and 30% left with a credit score below 670. The VA loan is specifically designed to work within these realities.

Understanding the VA loan benefit starts with a Certificate of Eligibility (COE), which confirms to lenders that a Veteran meets the service requirements for the VA home loan program. Veterans can request a COE through VA.gov or directly through a VA-approved lender.

From there, the critical step is working with a lender who has genuine VA loan experience. Not all lenders handle VA loans with the same depth of knowledge. A lender who specializes in VA loans will know how to count BAH correctly, explain the funding fee, identify whether a Veteran qualifies for a funding fee exemption due to a service-connected disability, and guide the borrower through property requirements without unnecessary delays.

The VA loan is not a last-resort option. It is a strategic financial tool built around the realities of military service and designed to lower the cost of homeownership for those who have earned it.

Ready to find out more about VA loans? Learn more at NewDay USA.

Methodology

On behalf of NewDay USA, data and research firm Researchscape conducted an online survey of 1,238 current and former U.S. military service members between February 18 and March 7, 2026. Respondents were recruited from a variety of sources to ensure a diverse sample, including:

- Panels

- Apps

- Websites

- Reward programs

Precision is estimated using a credibility interval of plus or minus 4 percentage points for questions answered by all respondents.

FAQs

Do VA loans really offer no down payment?

Yes. Eligible Veterans can purchase a home with no down payment through the VA home loan program, which allows financing of up to 100% of the home's purchase price. Individual lenders may have their own requirements, so it is worth confirming directly with your lender.

Can BAH count as income when qualifying for a VA loan?

Yes. Basic Allowance for Housing is a recognized income source for VA loan qualification. Because it is not subject to federal income tax, many lenders will also gross it up, calculating its pre-tax equivalent value, which can increase the amount you qualify for.

Does a VA loan require private mortgage insurance (PMI)?

No. VA loans do not require PMI at any down payment level. The VA's guaranty to the lender replaces the role that PMI would otherwise serve, which can save borrowers hundreds of dollars per month compared to a conventional loan with less than 20% down.

How many times can a Veteran use the VA home loan benefit?

There is no limit on how many times an eligible Veteran can use the VA home loan benefit. Entitlement can be restored after a VA loan is paid off, allowing the benefit to be used multiple times over a lifetime.

What credit score is needed for a VA loan?

The VA does not set a minimum credit score requirement for its home loan program. Individual lenders establish their own benchmarks. Many VA-focused lenders work with scores in the mid-600s, though higher scores typically result in more competitive rate offers.