Condos can be a great entry point into homeownership, especially in urban areas where single-family homes may be financially out of reach. But if you're a Veteran hoping to use your VA loan benefit to purchase a condo, you'll need to navigate some additional requirements. You can use a VA loan to buy a condo, but the condo complex must be on the VA's approved list or go through an individual condo approval process, and the property must meet VA requirements for safety and soundness.

This guide walks you through everything you need to know about buying a condo with a VA loan, from understanding approval requirements to closing on your new home.

Why Condo Approval Matters

Unlike single-family homes, which only need to meet property requirements, condos come with an extra layer of scrutiny. The VA wants to ensure the entire condominium project is financially stable and properly managed, not just that your individual unit is in good shape.

Condo approval protects both you and the VA from several risks. A poorly managed HOA can leave you facing special assessments for major repairs. Financial instability in the condo association could affect your unit's value. Inadequate reserves might mean deferred maintenance that becomes your problem.

The approval process verifies that the condo association maintains proper insurance, keeps adequate financial reserves, follows sound management practices, and maintains the property appropriately. Think of it as the VA doing due diligence on your behalf to ensure you're buying into a well-run community.

Two Paths to Approval

There are two ways a condo can qualify for VA financing, and understanding both helps you know what to look for during your home search.

Project approval means the entire condo complex has been vetted and approved by the VA. Any unit within an approved project automatically qualifies for VA financing, assuming the individual unit meets property requirements. This is the smoothest, fastest path to purchasing a condo with your VA benefit.

Individual condo approval (sometimes called spot approval) is the alternative when a project isn't on the approved list. With this option, you can request approval for your specific unit and transaction. The VA evaluates both your particular unit and the overall project health to determine if they'll guarantee a loan for this purchase.

Individual approval only covers your specific transaction. If another Veteran wants to buy a different unit in the same building later, they'll need to go through the process again unless the project pursues full approval.

Checking if a Condo is VA-Approved

Before you fall in love with a specific condo, check its approval status. The VA maintains a searchable database of approved condominium projects. You can search by project name, address, or location to see if a condo complex has current VA approval. Approval status changes over time. Projects get added when developers or HOAs submit applications, and approvals expire if not renewed. Always check the expiration date on any approval. If it's expired or expiring soon, the project will need to go through reapproval before your loan can close.

Share your financing type with your real estate agent from the beginning. Experienced agents familiar with VA loans can help you focus on approved properties or identify good candidates for spot approval. They can also contact listing agents to verify approval status before you make an offer.

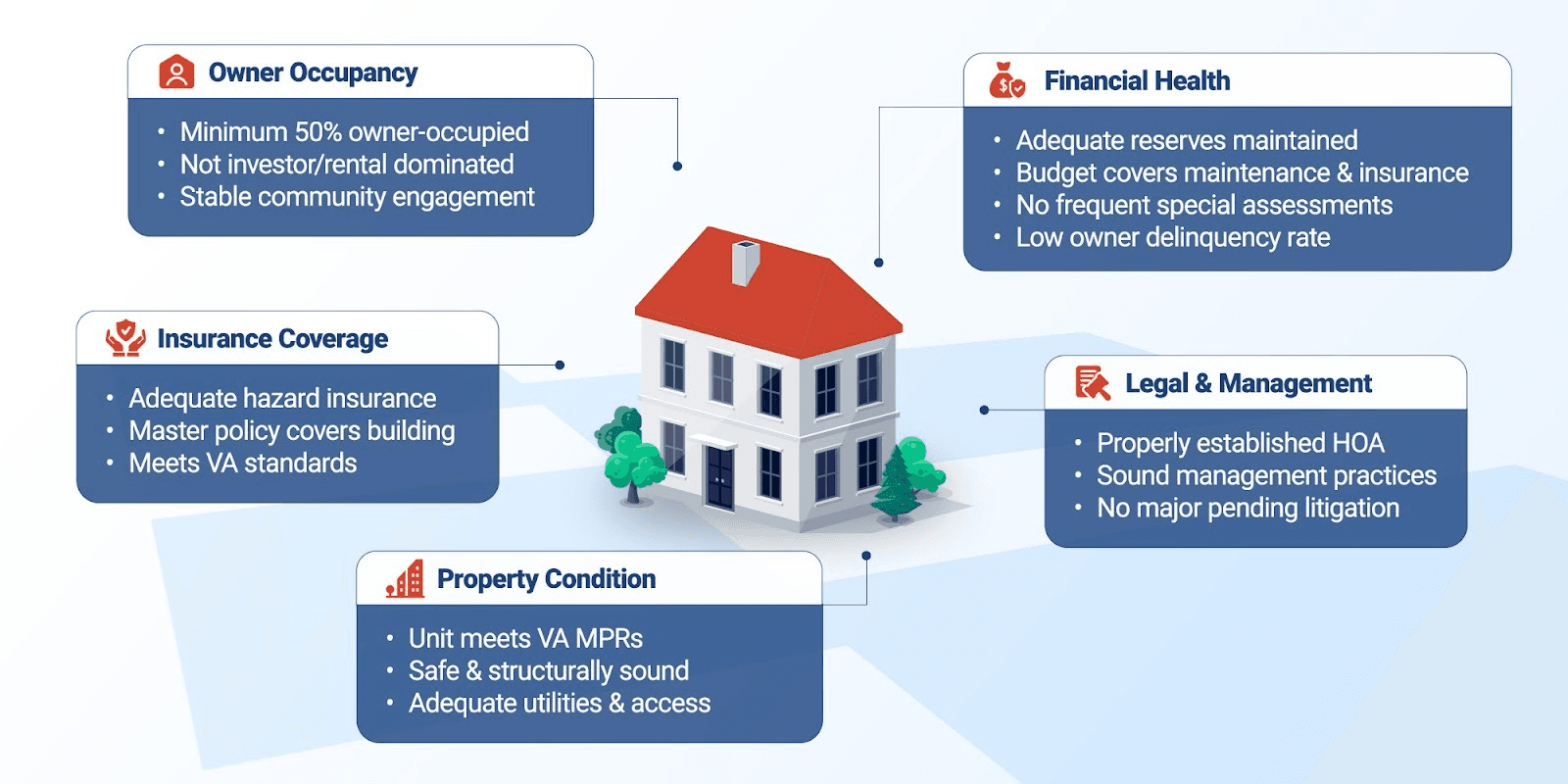

Requirements for VA Condo Approval

Image created for NewDay USA

Whether pursuing project or individual approval, certain criteria must be met.

Financial Health of the HOA

The condo association must maintain adequate financial reserves to ensure the HOA can handle unexpected expenses without immediately hitting owners with special assessments. The HOA should have a budget that covers ongoing maintenance, insurance, professional management if applicable, and contributions to reserves.

Lenders review recent financial statements to assess the association's fiscal health. Red flags include consistently depleted reserves, frequent special assessments, or unpaid bills and delinquent owners.

Owner Occupancy Requirements

The VA generally requires that at least 50% of units be owner-occupied rather than rentals. This requirement helps ensure a stable community where owners have a vested interest in maintaining property values and supporting sound management. Buildings dominated by rentals can potentially experience higher turnover and less community engagement.

Some exceptions exist for newer projects still selling initial units or buildings in resort areas, but the owner-occupancy ratio is a key consideration in most cases.

Insurance Coverage

The condo association must maintain adequate hazard insurance covering the building and common areas. The policy must meet VA standards for coverage. Individual unit owners typically carry their own HO-6 insurance covering personal property and improvements inside the unit, but the master policy covering the building itself needs to be comprehensive and current.

Legal and Management Standards

The condo must be legally established and properly managed. The VA also looks at whether the association is involved in significant litigation, as ongoing lawsuits can indicate serious problems with the property or management.

Property Condition

Even if the project meets financial and management requirements, individual units must still meet VA Minimum Property Requirements (MPRs. The unit must be safe, structurally sound, and have adequate utilities and access. Any deficiencies identified during appraisal will need to be addressed before closing.

Step-by-Step Process for Buying a Condo with a VA Loan

Once you understand the requirements, follow these steps to successfully purchase a condo using your VA benefit.

Step 1: Get Pre-Qualified or Pre-Approved

Before house hunting, get pre-qualified or pre-approved for a VA loan. This involves providing financial information to your lender, who reviews your credit, income, and VA eligibility to determine how much you can borrow.

Pre-approval strengthens your offer and shows sellers you're a serious buyer who can close the transaction. Have your Certificate of Eligibility (COE) ready, which you can obtain online through the VA portal, through your lender, or by mail.

Step 2: Find a Condo and Verify Approval Status

Work with your real estate agent to find condos that meet your needs and budget. For each property you're seriously considering, verify its VA approval status using the database.

Consider factors beyond just the unit itself. Research the HOA's reputation, review the monthly fees and what they include, check if the building has any planned major projects or assessments, and evaluate the location and overall community.

Step 3: Make an Offer

When you're ready to make an offer, ensure your purchase agreement includes appropriate contingencies. At minimum, include a financing contingency that allows you to cancel if you can't obtain VA financing, and an appraisal contingency that lets you walk away if the property doesn't appraise for the purchase price or doesn't meet VA requirements.

Step 4: Individual Approval Process (If Needed)

If you're pursuing individual approval, your lender will request documentation from the HOA, including recent financial statements and budgets, proof of adequate insurance coverage, owner-occupancy information, copies of declarations, bylaws, and rules, and information about any pending litigation or special assessments.

Step 5: Home Inspection and Appraisal

Consider ordering a home inspection even though it's not required. Inspectors examine your unit and can identify issues the appraisal might miss. This protects you from unpleasant surprises after moving in. In a condo, inspectors look at the unit's interior systems, appliances, and fixtures, as well as any exclusive-use areas like patios or balconies.

The VA appraisal assesses both value and condition. The appraiser will verify the unit meets MPRs and note any required repairs. They'll also confirm the condo approval status and may review HOA documents to ensure everything is in order.

Step 6: Review Condo Documents Carefully

Before closing, carefully review all condo association documents. Pay particular attention to monthly HOA fees, rules about rentals (if you might rent it out later), pet policies, parking arrangements, and any restrictions on modifications.

Some associations have rules that might not work for your lifestyle. Better to discover anything that may not work for you, before you buy than after you move in.

Step 7: Final Walkthrough and Closing

Conduct a final walkthrough shortly before closing to ensure the unit is in the agreed-upon condition and any required repairs have been completed. Verify that appliances and systems function properly.

At closing, you'll sign loan documents, pay closing costs (though remember VA loans don't require a down payment), and receive the keys to your new home. Your lender will explain all documents and answer any final questions.

Advantages of Buying a Condo with a VA Loan

Using a VA loan for a condo purchase offers significant benefits that conventional financing can't match.

You'll avoid the down payment that conventional loans typically require for condos. VA loans may allow zero down payment on approved condos. You won't pay private mortgage insurance (PMI), which conventional buyers must pay when putting down less than 20%. This saves you hundreds of dollars monthly.

Potential Challenges and How to Handle Them

Be prepared for a few challenges unique to condo purchases with VA loans.

Limited inventory: Not all condos are VA-approved, which narrows your options. Start your search knowing this and be prepared to either focus on approved buildings or pursue individual approval.

HOA cooperation: Individual approval requires cooperation from the HOA to provide documentation. Some associations are responsive and helpful, while others work slowly. Your lender can help navigate this process.

Timing: Individual approval adds time to the transaction. Make sure your purchase agreement allows sufficient time for this process.

Competing offers: In competitive markets, sellers sometimes prefer conventional buyers who don't need condo approval, seeing them as more certain to close. A strong pre-approval letter and earnest money deposit can help counter this concern.

Making Condo Ownership a Reality

Buying a condo with a VA loan is absolutely possible and can be an excellent path to homeownership. With preparation and the right team supporting you, you can successfully purchase a condo that meets your needs and makes smart use of your valuable VA benefit. Read more, and explore your options for condo ownership with VA financing.

FAQs

Can I buy any condo with a VA loan?

The condo must be either on the VA's approved project list or qualify for individual condo approval. Not all condos meet VA requirements for financial stability, owner-occupancy ratios, or management standards. Check the VA's condo database before making an offer.

How long does individual condo approval take?

Individual approval typically takes 2-4 weeks from when your lender submits the required documentation. The timeline depends on how quickly the HOA provides information and how busy the VA's approval team is. Build this time into your purchase contract to avoid rushing or missing deadlines.

What if the condo approval expires before I close?

If a project's approval expires before your closing date, the HOA or your lender can request renewal. Don't wait until the last minute. If you're making an offer on a condo with approval expiring soon, address this upfront and ensure renewal is handled before you get too far into the process.

Are there limits on condo prices with VA loans?

VA loan limits vary by county. Veterans with full entitlement can borrow up to these amounts with no down payment. Check the VA's loan limit page for your specific county.

Can I rent out a condo I bought with a VA loan?

VA loans require you to occupy the property as your primary residence. After you've lived there and met the occupancy requirement, you can rent it out if you have qualifying reasons for moving. Check with your lender about occupancy requirements.