Getting pre-approved for a VA home loan with NewDay USA means working with a lender that understands military timelines, military pay, and the realities of buying a home with orders pending or a retirement date on the calendar. Michael Ray, a retired U.S. Army Special Forces Veteran who served 22 years, experienced that firsthand when he used his VA benefit for the first time on his third home purchase.

The pre-approval process is designed around the way service members and Veterans actually live, not retrofitted from a civilian template. That focus shapes how a Veteran's Certificate of Eligibility gets pulled, how military income is reviewed, and how options like the NewDay Home Advantage Loan are layered in to fit a real-world buying timeline.

What VA Loan Pre-Approval Is

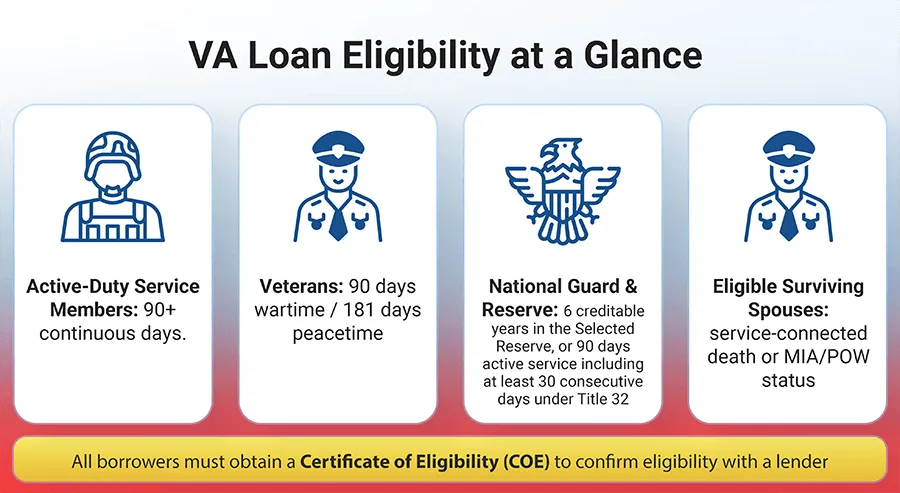

Pre-approval is a lender's documented assessment of what you can borrow, based on a review of your credit, income, assets, and verified VA eligibility. For Veterans, it includes pulling the Certificate of Eligibility (COE), the document that confirms to the lender that you qualify for VA-backed financing. According to the Department of Veterans Affairs, you can request your COE online, through your lender, or by mail.

Pre-qualification and pre-approval get confused all the time, but they aren't the same thing. Pre-qualification is a quick estimate based on numbers you share verbally. Pre-approval is documented and underwriting-reviewed. In a competitive market, sellers treat a pre-approval letter as evidence that you can actually close, and that's often what separates a winning offer from one that gets passed over.

Why Military Life Demands a Different Approach

Civilian buyers usually shop at their own pace. Military families rarely get that luxury. Permanent Change of Station (PCS) orders, retirement timing, end-of-lease deadlines, and deployment schedules all compress the decision window. A pre-approval process built around military life recognizes those pressures from the first phone call.

Tight Closing Windows

VA borrowers generally need to occupy the home within 60 days of closing, with extensions available in specific circumstances such as active deployment. That puts pre-approval under real pressure. By the time orders arrive, the clock is already running, and back-and-forth over paperwork can put a transaction at risk.

Military Pay Requires Specialized Review

Loan officers who don't work with military borrowers regularly can miss income that legitimately counts toward qualification. Basic Allowance for Housing (BAH), Basic Allowance for Subsistence (BAS), special pay, and combat pay all factor into how much a service member can borrow. Documentation comes from Leave and Earnings Statements (LES) and statements of service, not the standard W-2 packet that a typical underwriter is used to. A lender that handles VA loans every day reads those documents fluently.

A Real Veteran's Experience

Michael Ray, a retired U.S. Army Special Forces Veteran who served 22 years from 1971 to 1993, recently used NewDay USA for his third home purchase. His first two homes were financed with conventional loans. This time around, he chose to use his VA loan benefit for the first time, and he described the experience as seamless. His advice to other Veterans was direct: don't make a decision until you fully check out the VA, because the benefits are definitely there.

What stood out to Michael was something a lot of Veterans recognize once they're on the other side of it. He'd been in the military for more than two decades and out of it for nearly three more, and he said he'd learned more about Veterans' benefits in the past five years than he ever knew during his service or in the years after. That gap between earned benefits and known benefits is exactly what a military-focused pre-approval process is designed to close.

"Don't make a decision until you fully check out the VA. Make sure you look into it, because the benefits are definitely there. Don't sell the VA loan short. It's here for us. Use it, because it works." — Michael Ray, U.S. Army Special Forces Veteran

What Sets the NewDay USA Pre-Approval Process Apart

A few aspects of the NewDay USA process consistently come up in Veteran feedback.

Fast COE Retrieval

Lenders with direct access to the VA's WebLGY portal can often retrieve a Veteran's eligibility electronically. According to the VA's lender user guide, the automated system can issue a COE immediately when sufficient service information is on file. Veterans who request the COE on their own through VA.gov or by mail can sometimes wait significantly longer. Having the lender pull it on the front end removes a step that often holds up first-time VA buyers.

Pre-Approval

A Veteran's borrowing power often involves more than base salary. The pre-approval process reviews qualifying military income, considers how the VA funding fee affects loan amount, and accounts for funding fee exemptions. Veterans receiving compensation for a service-connected disability, or those eligible to receive it, are typically exempt from the funding fee entirely, which can change what a borrower qualifies for.

Bridging Gaps with the NewDay Home Advantage Loan

One of the most common pre-approval challenges for Veterans buying a new home before selling the current one is timing. Selling first usually means renting in between. Buying first usually means carrying two mortgages. The NewDay Home Advantage Loan, a companion personal loan offered alongside the VA mortgage, gives borrowers a way to cover closing costs and bridge that timing gap, with interest refunded if the personal loan is repaid within one year.

For Michael Ray, the Advantage Loan was the difference between being able to move forward and having to wait. He and his wife were selling their current home and didn't want to lose time renting in between. Without the Advantage Loan, he said, he wouldn't have been able to buy the home he wanted on his timeline.

Common Misconceptions That Slow Veterans Down

Misconceptions about the VA loan are still everywhere, and they often come from professionals who should know better. The VA's quick reference for real estate professionals addresses several of the most common ones.

- VA loans take too long to close. The VA reports that closing times are competitive with conventional and FHA loans.

- VA loans require a down payment. They generally don't, as long as the sales price doesn't exceed the appraised value.

- The COE process is slow. Most lenders can pull a COE electronically, often the same day.

- VA loans don't work for condos. They do, as long as the development is on the VA's approved condo list.

The pattern shows up consistently across all four. Veterans who haven't used their benefit often don't know what's possible, and the professionals around them sometimes don't either. That's a knowledge gap a military-focused lender is positioned to close before it costs a Veteran a home.

How to Prepare for VA Loan Pre-Approval

A few practical steps make the pre-approval phase smoother and faster.

- Gather your service documentation. For Veterans, that means a DD-214. For active-duty service members, a statement of service from your command works.

- Pull your most recent LES or pay stubs, plus two years of W-2s or tax returns or any other income documentation.

- Have asset documentation ready, including bank statements and any retirement accounts.

- Avoid opening new credit lines or making large purchases during the pre-approval process. New debt changes your debt-to-income ratio.

- Be upfront about timing. If you're under a PCS deadline or end-of-lease pressure, tell your loan officer early. That information shapes how the file moves.

Read more about VA loans and how to put your earned benefit to work.

Military-Focused Pre-Approval

Service documentation pulled first. DD-214 for Veterans, statement of service for active duty, ready before anything else.

Certificate of Eligibility retrieved electronically. With lender access to WebLGY, eligibility can often be confirmed the same day rather than waiting on a mailed request.

Military income reviewed in full. BAH, BAS, special pay, and combat pay all factored in, with LES and statement-of-service documentation read fluently.

Funding fee status confirmed. Service-connected disability exemptions identified up front, since they change what a borrower qualifies for.

Advantage Loan considered where it fits. For borrowers selling one home and buying another, the companion personal loan bridges closing costs without draining savings.

Pre-approval letter issued. Documented, underwriting-reviewed, and ready for a competitive offer.

FAQs

What income counts toward VA loan qualification?

Military income sources like BAH, BAS, and special pay all count, and lenders who handle VA loans daily know how to document and verify them correctly.

How long does it take to get a Certificate of Eligibility?

Lenders with access to the VA's WebLGY portal can often pull your COE electronically the same day, far faster than requesting it yourself.

What if I'm buying a new home before my current one sells?

The NewDay Home Advantage Loan can cover closing costs and bridge the gap between buying and selling, with interest refunded if repaid within one year.

Do Veterans with a service-connected disability have to pay the VA funding fee?

No. Veterans receiving service-connected disability compensation are typically exempt, which can meaningfully affect how much you qualify to borrow.